Discover the essential steps to power your online payments with Solidgate solutions, built with businesses and their challenges in mind. Gain a strong understanding of transaction flows and key aspects of payment processing, including

Glossary

A security protocol for online transactions, adding an extra layer of authentication. Customers may receive a one-time code for verification, reducing the risk of unauthorized transactions.

3D Secure

authentication and

Glossary

The return of funds to a customer, typically for a returned or cancelled purchase.

refunds.

Take control of your business operations with the Solidgate Hub, managing payments and products while building customer trust and loyalty with every interaction.

Integrate

Solidgate offers multiple integration options to meet different business needs.

Solidgate

API

allows businesses to integrate and customize solutions to meet specific requirements. Meanwhile,

Solidgate

SDK

simplifies integration by providing

Glossary

The process of replacing sensitive data with a unique identifier, token, for enhanced security.

token generation

and secure transaction handling.

Solidgate’s host-to-host integration gives merchants complete control over their checkout page, allowing for customization and effective management of the payment process. With the use of digital wallets and alternative payment methods, businesses can increase

Glossary

Metrics that indicate the percentage of customers who successfully complete the payment process once they have initiated it.

conversion rates

and meet the unique preferences of customers in different locations.

Glossary

An interface allowing customers to input payment details for a transaction.

Payment form,

Glossary

A web page where customers enter payment details to complete a transaction.

payment page,

and e-commerce plugins provide customer-friendly and secure payment options, simplifying transaction processing. You can customize them to match your brand and meet regional requirements.

Learn about the steps of the Payment Form integration flow to successfully configure the checkout:

- Backend configuration

- SDK installation

- API instance creation

- Merchant data management

You can customize the payment form for region-specific customer experiences, add buttons for digital wallets, and collect additional fields required for specific transactions.

In addition to straightforward integration, Payment Page supports customizable elements to enhance the customer journey:

- Brand logo and colors

- Public merchant name

- Order descriptions

- Support for multiple payment methods

You can provide customers with global options like card payments and digital wallets, alongside local methods like iDeal or Blik, ensuring an efficient checkout experience.

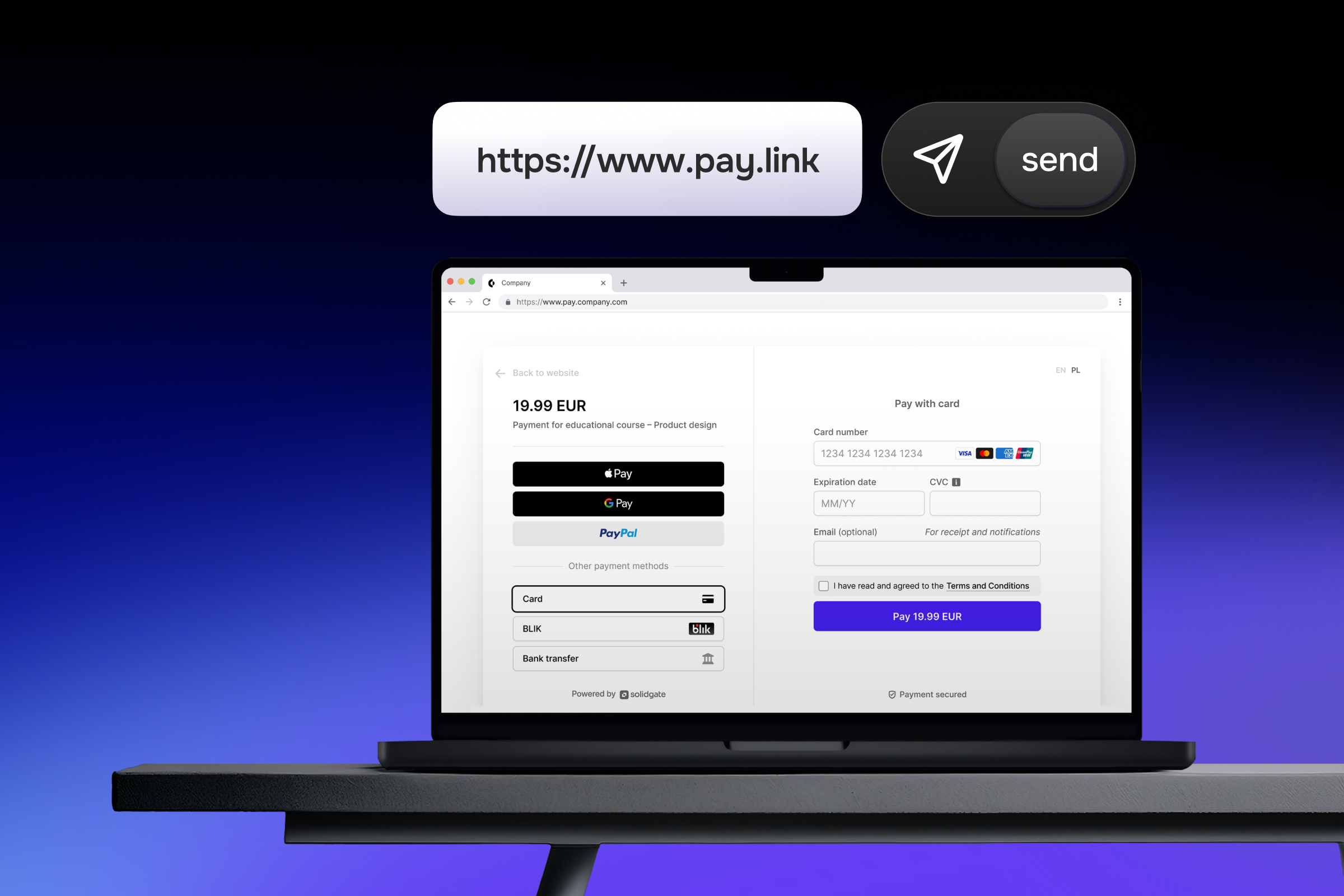

After generating your Payment Link URL, you can share it with customers across multiple channels:

- Embed directly in a website button

- Include in abandoned cart communications

- Send directly via email or SMS

- Share on social media platforms

Once created, the payment link can be shared repeatedly. The link is highly reusable, allowing customers to retry payments after a decline to recover lost sales.

It provides multiple API types for different transactions, simplifying operations for merchants. Key aspects include:

- Authorization, settlement, and refunds

- Payments without CVV requirements

- Zero-amount authorization flows

- Retry logic to increase conversion rates

Note that only PCI DSS certified merchants are eligible for full API access, as they must securely collect card data and host their own payment form.

Launch

Testing integration, using

Glossary

A mechanism enabling real-time communication and data exchange between different systems to notify about specific events or updates.

webhooks,

understanding error codes, and ensuring compliance with industry legal and regulatory requirements are all essential aspects of a successful payment system integration for merchants.

Non-traditional payment methods beyond credit cards, such as bank transfers. alternative payments, Glossary

A payment arrangement where a customer authorizes the automatic and periodic withdrawal of funds from their account to fulfill ongoing financial obligations. subscriptions, Glossary

A dispute process initiated by a cardholder, resulting in the reversal of a transaction and funds returned. chargebacks, and Glossary

It involves a notification about an unauthorized transaction due to stolen payment or identity information, causing financial losses. fraud alerts.

A code indicating the reason for the rejection of a transaction. error code, you can provide specific instructions to resolve the issue. Knowing common decline codes like Guide

The general group of declines. The card-issuing bank did not complete the transaction successfully. 0.01 General decline or Guide

The payment was not completed within the allocated timeframe, leading to order expiration. 0.02 Order expired helps guide customers toward successfully completing their transactions.

Manage

Solidgate Hub centralizes payment and operational processes, providing tools and actionable insights to handle and improve key aspects of online business management.

With the Solidgate Hub, you can optimize payment and product management, refining processes that drive growth and help you build customer trust. Use its analytics and reporting to get valuable insights into transactions and financial health. Secure your operations with flexible role management, giving team members exactly the access they need based on your organizational structure.